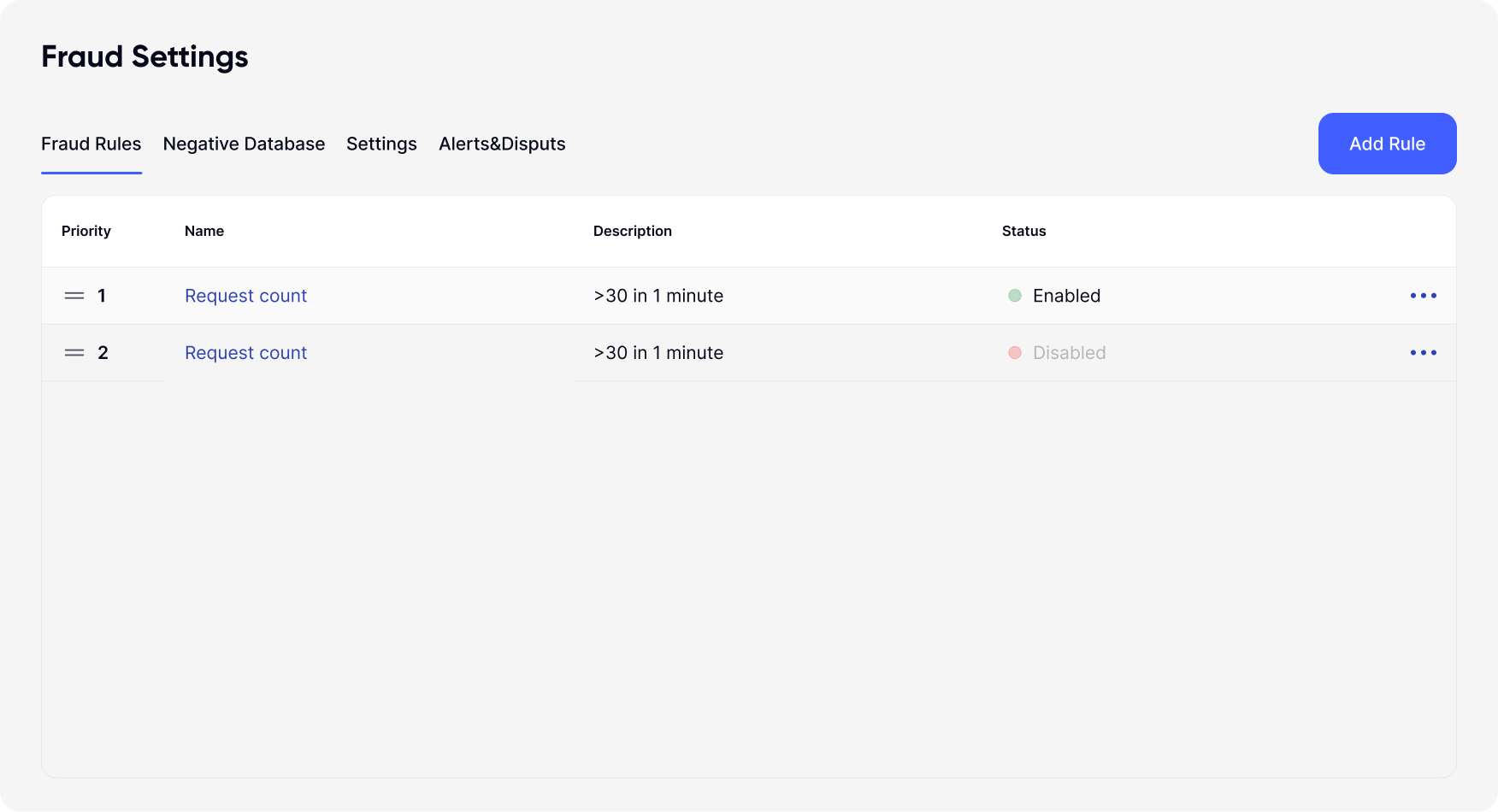

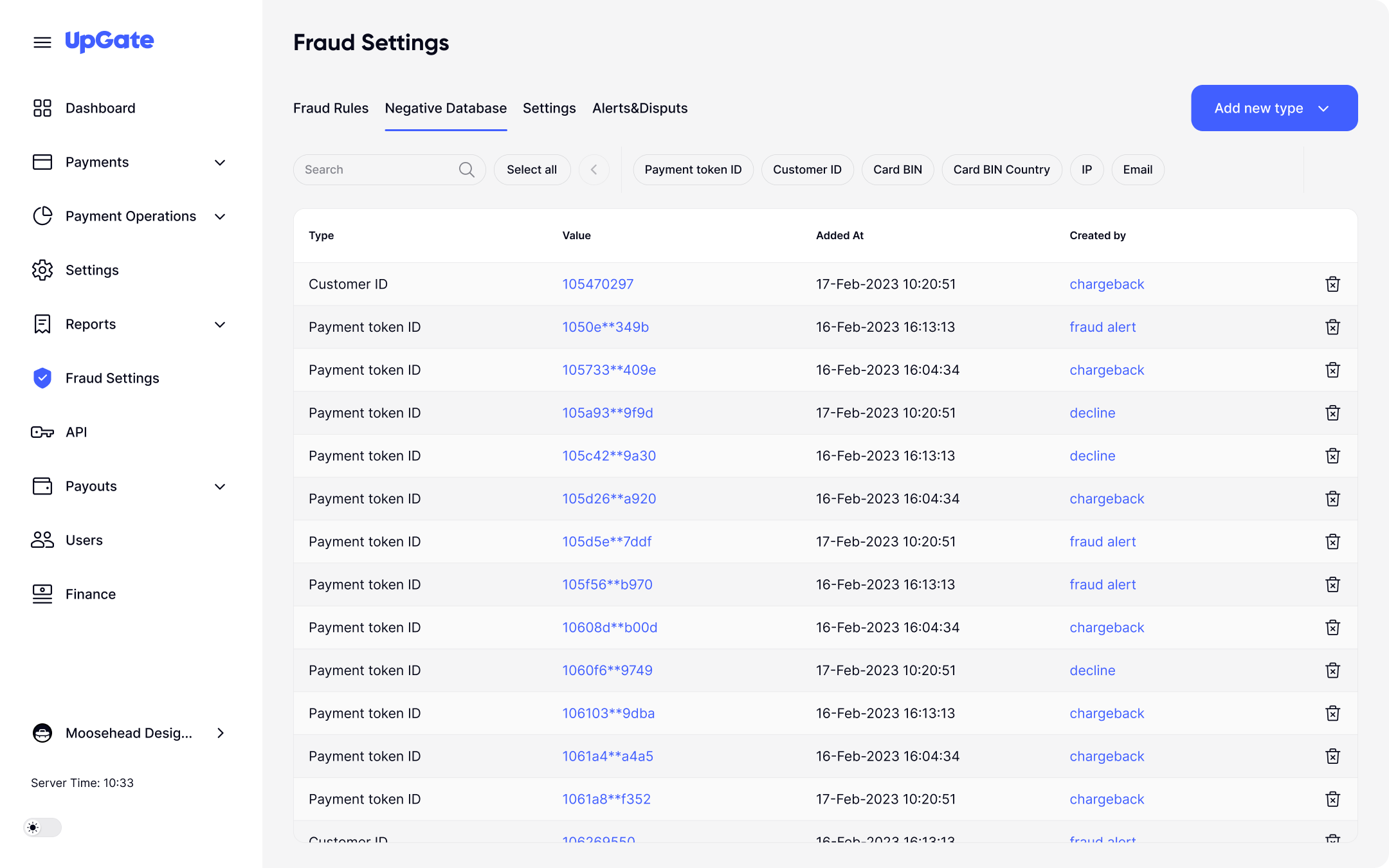

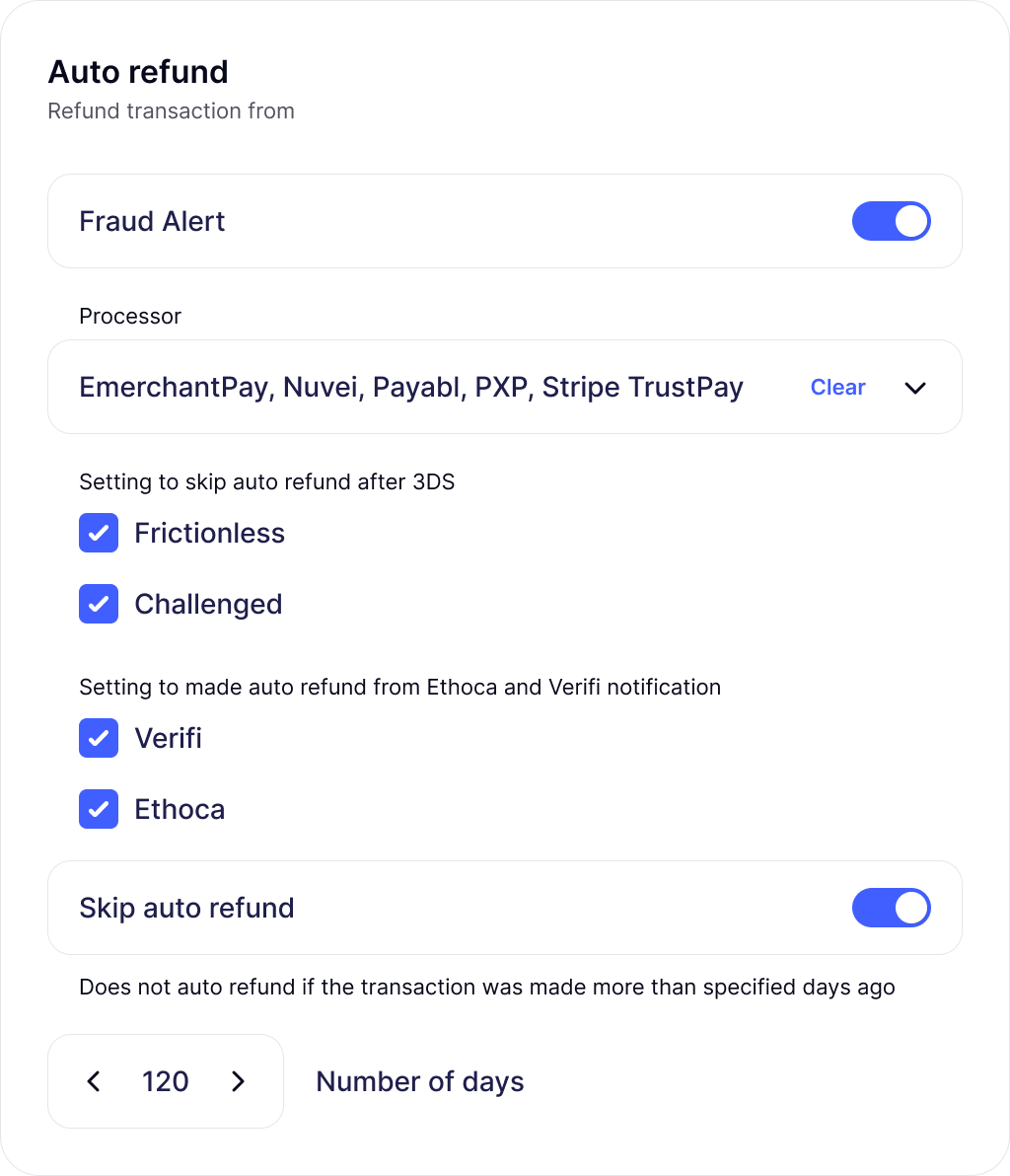

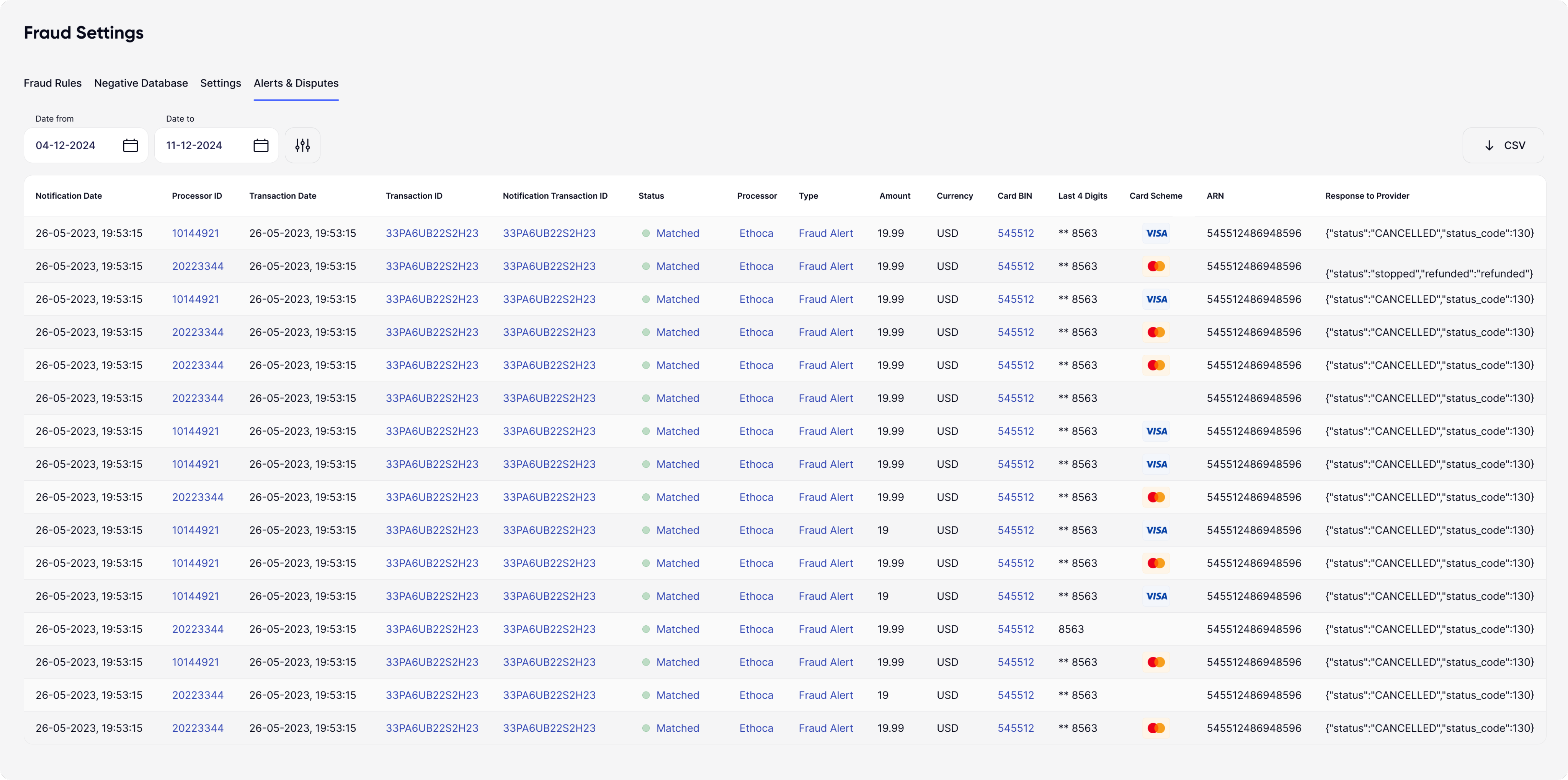

UpGate Risk Engine — Fraud Prevention at the Orchestration Layer

UpGate provides a single, consistent fraud evaluation layer before a transaction is routed to any payment processor. This eliminates fragmented risk logic, inconsistent decline patterns and the ability for fraudsters to bypass controls by switching processors.

All fraud rules, alerts, and actions are evaluated centrally — ensuring predictable protection and eliminating gaps caused by processor-level logic

Get started